Updated for 2019. When choosing a 529 college savings plan, you can open a 529 plan from any state. However, each state can vary widely in what they offer in terms of tax deductions and/or matching grants. You may have to weigh your in-state benefits against the superior investment options from an out-of-state plan. Morningstar has just published their , which included a state-by-state summary of the tax benefits:

Based on a , their conclusion is that if your in-state tax benefit is greater than 5% of your contribution, then you should stick with your in-state plan. For example, if you contribution $100 a month ($1,200 annually), the tax benefit should be at least $60 to offset the chance that another state has a plan with slightly lower annual costs.

If your potential in-state tax benefit is less than 5% of your contribution, then it is a close call. You should weigh various factors like relative fee amounts and quality of investment options. If your state does “tax parity” – meaning it offers the same tax benefits for any 529 plan – then you should simply choose the .

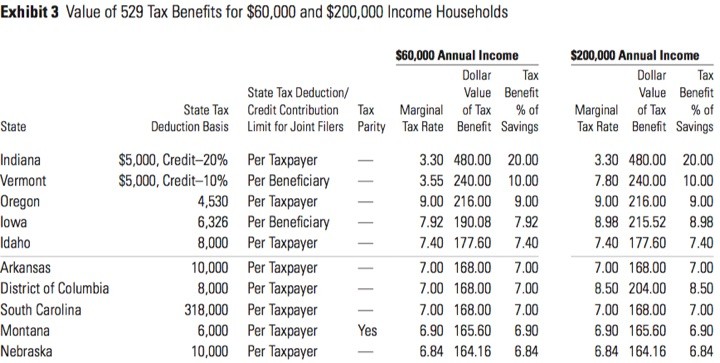

It’s hard to cover all possible situations, but here is an older 2015 chart that quantifies tax benefits for a hypothetical family saving for college (two adults, two children, $100 per month savings per child) at both the $60,000 and $200,000 household income levels. Tax breaks do change regularly, so I would double-check before making a contribution based on these numbers.

For reference, here’s an older chart from 2014:

My observation as someone who has been tracking these plans for several years is that many of the factors considered here are subject to change. State-specific tax breaks may come and go. 529 plan costs and investment options also change from year to year, with the overall trend being that the worst plans tend to get better due to competitive pressure. (No state wants to be the “worst” plan, and an expensive plan can switch administrators and transform into a cheap plan within a year.) Meanwhile, the top plans tend to stay that way.

Therefore, I would also consider trying to grab any significant tax break that is available now and hope that the plan gets better in the future. Some states even let you grab the tax deduction and then immediately roll over the assets to any outside plan; other states “recapture” the tax deduction if do you that within a certain time period. Sometimes you can wait out the recapture period and then roll funds over to a better state 529 plan for free (once every rolling 12 months).

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2018 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.