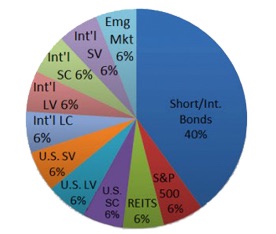

Some investors like to break down their investments into several different asset and sub-asset classes. For example, here is a pie chart showing the recommended by Paul Merriman. You don’t need to hold every one of these asset classes, this is just an example with a lot of “slices”.

Some investors like to break down their investments into several different asset and sub-asset classes. For example, here is a pie chart showing the recommended by Paul Merriman. You don’t need to hold every one of these asset classes, this is just an example with a lot of “slices”.

What is the best ETF to buy for each asset class? These days, there are multiple ETFs for nearly every sub-asset class or factor. The best ETF can depend on multiple factors, for example whether you buy it in a tax-deferred or taxable account. Established providers include Vanguard, iShares, Schwab, SPDR, and Invesco. (If you are planning to juggle this many ETFs, consider the automatic rebalancing “pie” feature of the brokerage firm .)

In the past, I have referred to this . As advisors affiliated with Dimensional Fund Advisors (DFA), they are able to use DFA mutual funds to build portfolios for their clients. Unfortunately, DFA mutual funds are not available to the public, and so we have to look for the best alternatives. The page is updated every so often.

Recently, I have found this . In 2021, Merriman started recommending a new provider of ETFs called Avantis, which was born when several DFA employees split off and formed their own company. Here is part of his rationale:

What’s changed is the inclusion of the five Avantis funds (AVUS, AVUV, AVDE, AVDV and AVEM). Avantis is relatively new to the ETF space, having been introduced a little over a year ago. The company was founded by former DFA employees and follows a philosophy very consistent with the design of Paul’s portfolios. Over the course of the past year, their funds have matured to where we decided it was time to include them in our evaluation.

Here are the recommended Avantis ETFs:

- Avantis US Equity ETF (AVUS)

- Avantis US Small Cap Value ETF (AVUV)

- Avantis International Equity ETF (AVDE)

- Avantis International Small Cap Value ETF (AVDV)

- Avantis Emerging Markets Equity ETF (AVEM)

DFA recently announced that they are also expanding into ETFs, which can be bought and sold by the general public in any brokerage account. These ETFs just started trading in late 2020:

- Dimensional US Core Equity Market ETF (DFAU)

- Dimensional International Core Equity Market ETF (DFAI)

- Dimensional Emerging Core Equity Market ETF (DFAE)

My own portfolio has only a little bit of this added complexity, with a goal of adding some extra exposure to asset classes with a relatively long history of high risk-adjusted returns. These are interesting developments if you also invest in this way, but I don’t necessarily recommend you do so, as I also agree with Merriman in this regard:

In the end, it’s probably more important that you have an investment strategy you believe in and can stick with than that you have exactly the right funds for that strategy.

Do your research, and find an investment strategy that fits with your psychological temperament and investment beliefs. Being able to “keep the faith” and stick with your strategy through the inevitable ups and downs is the most important thing. For example, even if dividend income investing isn’t academic-theory-optimal, it may be psychologically-optimal for many people and has successfully funded many comfortable retirements. For many other people, the best option is something that they can set-and-forget. Accordingly, many people can create a comfortable retirement with a .

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2004-2021 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.