Updated for crazy 2020. The big news yesterday was that one measure of crude oil prices actually , because futures were coming due and nobody had any place to store the oil upon delivery.

Why did this happen? The simple answer is that too many people had the following plan:

- Crude oil has dropped to $18 a barrel. These prices are multi-decade lows.

- Oil prices must go up again… eventually… right? Look at that historical chart!

- The futures market is kinda complicated… I know! I’ll buy an ETF like .

- Profit!?!?

Here are a few things you should know first about the United States Oil Fund (USO) and similar oil ETPs.

You aren’t the only one who’s thought of this. Billion of dollars have come and gone into oil ETFs in the past few years. Here are articles from 2014 and 2015 when oil dropped to below $50 a gallon after being over $100:

- (Nov 2014)

- (Jan 2015)

- (Jan 2015)

In April 2020, USO ended up having to actually in order to avoid some the market distortions that the speculation caused.

The usual market timing questions apply. Sure, the price will go up, but how long is “eventually”? It might be 1,3,5, or 10 years. If you have a specific time-frame in mind, then you can go out on the futures market and then buy a specific contract. But if oil hasn’t risen enough at that time – maybe it peaked earlier and dropped, or it peaks further in the future – you’ll have lost money.

If you buy the ETF, when is a good time to sell? $40 a barrel? $80? $100? What if you sell and then it rises another 50%?

What if it takes a while? The longer you have to hold these ETFs, the less likely they will track the price of oil (see below). Meanwhile, the ETF provider is happily collecting their annual expense ratios of 0.50% to 1%. At the current asset level of $4 billion times the 0.45% management fee, that’s $18 million a year in fees.

Your commodities futures ETF may not track the price of oil very well at all. To properly track the price of oil, you’d need to buy some oil and store it somewhere (and pay storage and security costs). These ETFs don’t do that, instead they buy oil futures contracts and keep rolling them over into new ones when they expire. That’s not the same thing. USO is designed to track daily price movements in the price of oil, not long-term movements!

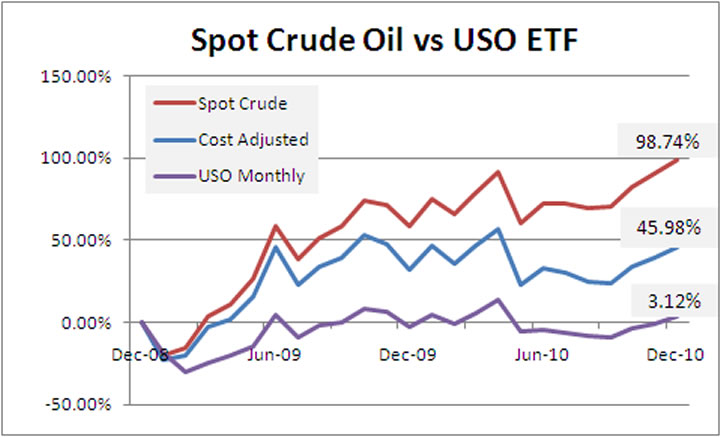

Oil prices doubled from in 2009-2010. USO went nowhere. Visually, here’s a chart from Attain Capital that compares the change in USO share price (purple) as compared to the spot price of crude oil (red) when oil prices doubled between the start of 2009 and the end of 2010 (blue line adjusts USO underperformance for roll costs):

From the Bloomberg article above:

Since USO launched in April 2006, it has returned -71 percent, while the spot price of oil returned -26 percent. The last time oil roared back from a bottom was in 2009, when it returned 78 percent on the year. USO returned just 14 percent.

If you don’t understand the terms “backwardation”, “contango”, and “roll costs” then you don’t understand commodities futures. If you don’t understand something, you probably shouldn’t buy it. The more people crowd into this trade, the weirder the futures markets get. Who would think that you could get paid to take oil from someone? Take it straight from a USO executive:

John Hyland, chief investment officer of USO, says the fund is a “tactical trading vehicle predominately used by professional traders,” and not meant to be a buy-and-hold investment.

In the end, such a play is a speculative bet and it may just pay off, who knows. But it certainly isn’t a wise investment, especially if the tool you’re using doesn’t even do what you want it to do.

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2019 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.

Related Posts