Update December 2021: On December 15th, 2021, HMBradley announced to their interest rate that will become effective February 1st, 2022, along with changes to their that are effective January 1st, 2022. Here are the old and new “no credit card” interest rates on balances up to $100,000:

Savings Tier APYs effective now through 1/31/2022:

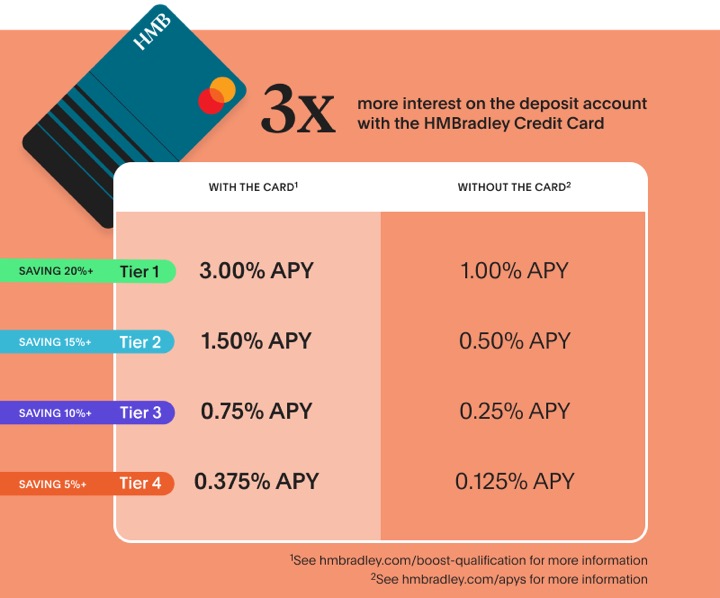

- Tier 1: 3.00% APY

- Tier 2: 2.00% APY

- Tier 3: 1.00% APY

- Tier 4: 0.50% APY

Savings Tier APYs effective 2/1/2022:

- Tier 1: 1.00% APY

- Tier 2: 0.50% APY

- Tier 3: 0.25% APY

- Tier 4: 0.125% APY

“3X with credit card” rates. As of 1/1/2022, if you spend at least $100 each monthly cycle on the HMBradley credit card AND have a least $2,500 in monthly direct deposits for each month of the previous quarter, then you can receive the following higher interest rates (3x):

(The Savings Tier Boost Promotion terms say this is effective starting 1/1/2022, but the e-mail sent out says it starts 2/1/2022 for existing credit card holders.)

For new customers, you will need to become an HMBradley credit cardholder first before being able to open the HMBradley interest-bearing checking account.

In realistic terms, an interest rate drop was coming sooner or later. 3% APY was amazing, but 1% APY is still double what most “high-yield” savings accounts offer. As someone who already uses their credit card, my interest rate is only going down from 3.5% APY to 3% APY. Read on getting approved either by increasing your direct deposit or self-reporting adequate income.

Spending $100 on the card per month is not bad, it’s probably the $2,500 monthly direct deposit that is slightly more problematic. Savings 20% of $2,500 means leaving $500 in there every month. However, since HMB credit card spend doesn’t count against the 20% savings requirements, you can simply put $500 on the credit card. I simply use my card for “online shopping” each money and earn 3% back on it as my top category, so there is no loss there. If HMB will pay me 3% APY on $100,000 (roughly $250 a month in interest), I will happily pay a $5/month annual fee for the credit card.

Quick take. As of 2/1/2022, HMBradly’s interest rates will drop significantly unless you utilize their HMBradley credit card. However, if you do have their credit card and meet the requirements, you can still earn up to 3% APY and the drop from before is not nearly as bad.

Original post (will be outdated as of 1/1/2022):

is a fintech bank startup that differs by offering customers a variable interest rate based on their savings rate. Deposits are FDIC-insured through Hatch Bank. As of July 2021, the top rate is 3% APY, which is over 2% higher than the popular online savings accounts like Ally Bank, Capital One, or Marcus. Is there a catch? What’s the fine print? Here’s my review of HMBradley after opening an account and reading their FAQ, fee schedule, and other fine print. Thanks to reader Guarav for the tip.

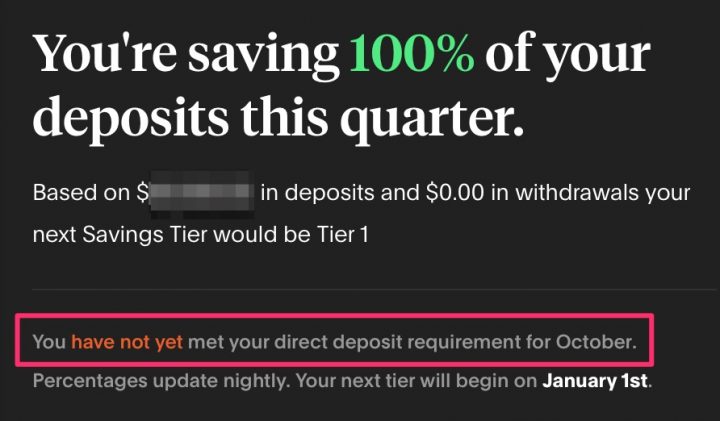

Rate tiers. Interest is earned on balances up to $100,000 and is set each calendar quarter. The interest rate updates for all customers at the beginning of each calendar quarter: January 1st, April 1st, July 1st, and October 1st. In order to qualify for a “Savings Tier”, you must receive a direct deposit at least once every month and save at least 5% of your quarterly deposits.

New customers start in Tier 3 and stay there as long as they maintain at least one direct deposit per month. For example, if you open in October, the next reset date would be January 1st and your interest earned for the next 3 months is based on your activity in the previous 3 months. Here are the current rates for each tier:

Requires a “real” direct deposit every month. You must receive some sort of direct deposit each month, as defined below:

For our accounts, we define direct deposits as those deposits made by the customer’s employer or a federal or state government agency or retirement benefits administrator. These generally include payments made by corporations and other organizations. We do not consider deposits to an account that are made by an individual using online banking or other payment provider such as PayPal or Venmo as direct deposits.

They appear to be relatively strict on receiving a “real” direct deposit and not a person-to-person transfer. Based on my experience, they have a system for detecting incoming deposits and marking them automatically as “real”, but it is not 100% accurate and your direct deposit may have to be reviewed manually. Their online account interface clearly tells you if you have made the required direct deposit for the current month (see screenshot below). If not, you should contact them in order for them to manually check and mark your transfer as a direct deposit. I have a legit employer direct deposit and had to ask them to manually review it. After that, they usually marked it as a direct deposit within 24-48 hours after arrive. (Due to the delay, I believe they still check manually.) Having it marked properly is required to get the top rate.

Savings rate is based on ALL deposits and withdrawals. For the calculation of “savings rate”, all deposits are considered including incoming transfers from another personal bank account. At the same time, your “spending” will also include any transfer out of your account, even if it’s just to another bank account that you own.

Basically, money has to keep coming into HMBradley and not go back out, if you maintain a positive savings rate. That’s rather clever. They just have to maintain the high interest rates to keep reinforcing this cycle.

NOW account? No paper checks. It should be noted that HM Bradley’s account is actually a lesser-known form called a “negotiable order of withdrawal (NOW) account”, which per the which gives the bank the right to require at least seven days written notice of a withdrawal. Supposedly, this is rarely done in practice. Like a checking account, there are no limits on the number of withdrawals each month. However, unlike a checking account… there are no checks! I suspect that not having to deal with paper checks saves them a good chunk of money. I’m personally fine with that as long that equates to a higher interest rate.

The Bank offers Negotiable Order of Withdrawal transaction checking accounts, which allows you to make deposits by check, ACH payment, transfer from another account at the Bank, or wire transfer. NOW accounts only are available to consumers for personal, family, or household purposes. The Bank does not offer business accounts and you agree not to use your HMBradley Account for business purposes. The Bank may request 7 days’ advance notice of a withdrawal or transfer of funds from the NOW account.

Credit card adds 0.50% APY. They recently added a credit card, but it is invite-only and based on their estimate of your income (which is in turn based on the size of your deposits, although you can attempt to self-report). See my . If you do get it, you can earn another additional 0.50% APY, for a total of up to 3.5% APY.

Additional features. No minimum balance, no monthly fees. $100 minimum to open. Interest is compounded daily and credited monthly. No paper checks. There is fee-free ATM access via your Debit Mastercard at over 55,000 ATMs in the STAR and MoneyPass networks (or at any store that allows for cash back on debit purchases). There is no online billpay (“coming soon”) and there is no ability to deposit checks (remote deposit also “coming soon”). They may close your account without notice if you maintain a zero balance.

My thoughts. In the current rate environment, the ability to earn 3% APY on up to $100,000 is exceptional. I don’t know of any “rewards checking” account has a balance limit of $100,000. This can be a good opportunity if you understand the rules and the top interest rate stays higher than the competition.

The idea of incentivized higher savings rates is good, but it may be a tough hurdle for those living paycheck-to-paycheck. On the other hand, as long as you can switch over a partial direct deposit, adding some consistent amount each month with minimal withdrawals would also work.

Bottom line. HMBradley is a digital bank startup that differs by offering customers a high rate (currently up to 3% APY) based on the percentage of their deposits that they save. They require moving over a monthly direct deposit, and the rules are a bit more complex than a simple online savings account, but if the rates hold steady it can be a very competitive offer for motivated savers.

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2004-2021 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.

Related Posts