Update 3/15/24: M1 just sent me the following e-mail:

We’ve decided to end our M1 Plus membership program. Our premium features will no longer require membership and will instead be available to everyone who builds and manages their wealth on M1.

Starting May 15, a $3 monthly platform fee will apply to clients with less than $10,000 in M1 assets or without an active Personal Loan. Each billing cycle will last 30 days—meeting platform requirements* at least one day during each cycle will ensure this fee is waived for you.

*You will be charged the $3 Monthly Platform Fee if at any point during the 30 days prior to program launch your total aggregate M1 Earn and Invest balances do not equal or exceed $10,000 or you do not have an active M1 Personal Loan.

This is basically free stuff for those with $10,000 invested, and a fee hike for all those with less than $10,000 invested and weren’t already paying for M1 Plus. I happen to be above the $10,000 balance threshold with my IRA contributions, but not an M1 Plus subscriber, and so the new “free” M1 Plus feature that I might take advantage of is the free custodial accounts for kids. I plan to give them the option for regular, dollar-based investments in Berkshire Hathaway shares (diversified, more gradual growth with no taxable dividends).

M1 has been regularly tinkering with their pricing structure and balance of free and premium features. They rolled out a rewards credit card linked to company ownership, which I don’t think really caught on. They seem to be trying to find something shiny that people will like. That’s too bad, because I still really like the core features of M1. Sometimes I feel like they should really just own that they are the “Get Rich Slow” brokerage, as opposed to Robinhood as the “Get Rich Now!… or Lose All Your Money” brokerage. I mean, how many M1 screenshots have you seen that look like :

If M1 offered excellent customer service, they could take funds from Vanguard as the go-to for DIY index fund investors.

Original review, somewhat edited to be current:

I’ve tried out my share of robo-advisors, which always sounded nice in theory but I eventually became disillusioned as they kept generating lot of unnecessary taxes every time they change their model portfolios to chase the latest and hottest trends. My favorite service for those that want a little extra help is one where I can pick my own custom target portfolio, but the robo still does the hard work: . Here’s a quick rundown of what makes them different:

- Fully customizable. You pick your own target asset allocation “pie”. (You can add ETFs or individual stocks.) You can simply copy one of the many model portfolios out there, or make your own custom pie as you like. You have full control! M1 handles the tedious stuff, like rebalancing or dividing a $100 contribution across 8 different ETFs.

- No commissions. Free stock/ETF trades with a low $100 initial minimum for taxable accounts and a $500 minimum opening amount for retirement accounts. After your initial deposit any amount greater than $10 can be deposited.

- Free with $10,000 balance. Otherwise $3/month. Most robo-advisors charge an annual management fee of 0.25% to 0.50% of assets, or force you to own something bad, like a lot of low-interest cash. (Looking at you, Schwab…)

- Free dynamic rebalancing. All new deposits (and withdrawals) will be invested (or sold) dynamically to bring your portfolio back toward your target asset allocation. M1 will also rebalance your entire portfolio back to the target allocation for you with a few clicks (for free) whenever you choose, on demand. You don’t need to do any math or .

- Fractional shares (dollar-based). For example, you can just set it to automatically invest $100 a month, and your full amount will be spread across multiple ETFs. Dollar-based transactions were one of the advantages of buying a mutual fund, but fractional shares solve this problem. ETFs are also usually more tax-efficient than mutual funds.

- Real brokerage account with off-the-shelf investments that you can move out. Some robo-advisors hold special, proprietary funds that you have to sell if you ever leave, possibly creating a big tax bill. (Looking at you, Fidelity…) M1 is built on a regular brokerage account, so you can move your Vanguard/iShares/Schwab ETFs and stock shares out to another broker whenever you want.

M1 Finance checks off nearly all the boxes of my brokerage wish list. I suppose the only thing they could add would be to have the high availability of knowledgeable customer service of a huge company like Fidelity or Schwab. Otherwise, I really like their feature set and I have been putting my recent annual IRA contributions into M1.

If you want to invest in newer factor ETFs that focus on Small-Cap, Value, Momentum, or Quality factors like those from DFA and Avantis, or a mix of dividend-oriented ETFs like SCHD/VIG/VYM, their service makes it much easier to set up a portfolio mix of different ETFs.

M1 Plus features are now available to everyone. M1 Plus was their premium subscription tier with several additional perks. Now everyone gets these features, but they are only free with a $10,000 balance and $3/month otherwise.

- High-yield savings (currently 5.00% APY as of 1/10/24). FDIC-insured up to $5 million.

- M1 Owner’s Rewards credit card (2.5%, 5%, or 10% cash back at 70+ brands, no annual fee).

- Lower interest rates on margin borrowing (1.5% rate discount).

- Custodial accounts for kids.

- Extra 3pm PM ET trade window.

- Automated “smart” transfers.

$100 referral bonus. M1 has a $100 referral bonus if you open a new account with $10,000 and maintain it for 30 days. You’ll also get 6 months free of their M1 Plus premium service. Here are the . Here is (thanks if you use it!) from which you must start opening your new account.

A bonus that amounts to 1% of your initial deposit with only a 30 day hold is technically a 12% annualized yield. This is also better than their standard offer for a $10,000 new deposit (see below), and you can also consider the ACAT transfer and retirement rollover promos below.

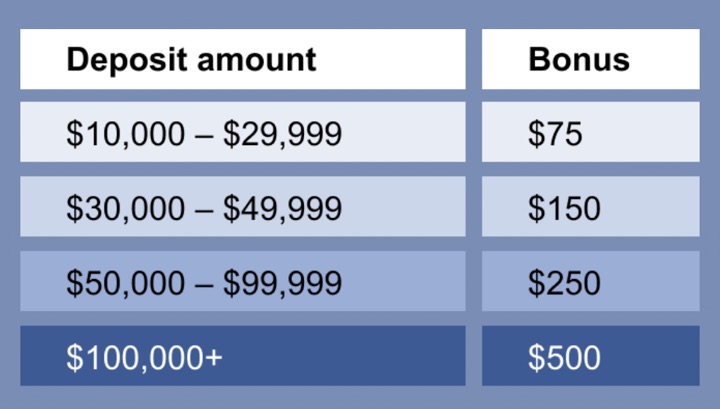

Up to $500 New User deposit bonus. Deposit $10,000 or more within two weeks of opening your new M1 Brokerage Account and get a cash bonus of $75 – $500 deposited to that account. See for full details.

Up to $20,000 ACAT Transfer bonus. You can get up to $20,000 when you

transfer brokerage assets via ACAT to M1 by 3/31/2024. See for full details.

Up to $5,000 Retirement Rollover bonus. You can get up to $5,000 when you

roll over your 401(k), 403(b) or another employer-sponsored retirement plan in an M1 Traditional/Roth IRA account by 3/31/2024. See this for full details.

Bottom line. is a brokerage account that acts like a customizable robo-advisor with automatic rebalancing into a target portfolio. You control the model portfolio, and they do the tedious work. Great for implementation of a low-cost, index or passive ETF portfolio. New pricing structure as of May 15th, 2024: Free for those with $10,000 in assets, otherwise $3 a month.

Disclosure: If you use my referral link, I may be compensated if you click through my link and open a new account.

Also see:

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2004-2022 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.

Related Posts