The Paycheck Protection Program (PPP) got a lot of media attention when it first came out, but I feel that that attention has waned. Many PPP loan recipients are self-employed workers, sole proprietors, and/or independent contracts that file a Schedule C (or are single-person LLCs and S-Corps) and got a relatively modest loan amount. I am not an accountant, but here are some quick updates focused on that group:

The Paycheck Protection Program (PPP) got a lot of media attention when it first came out, but I feel that that attention has waned. Many PPP loan recipients are self-employed workers, sole proprietors, and/or independent contracts that file a Schedule C (or are single-person LLCs and S-Corps) and got a relatively modest loan amount. I am not an accountant, but here are some quick updates focused on that group:

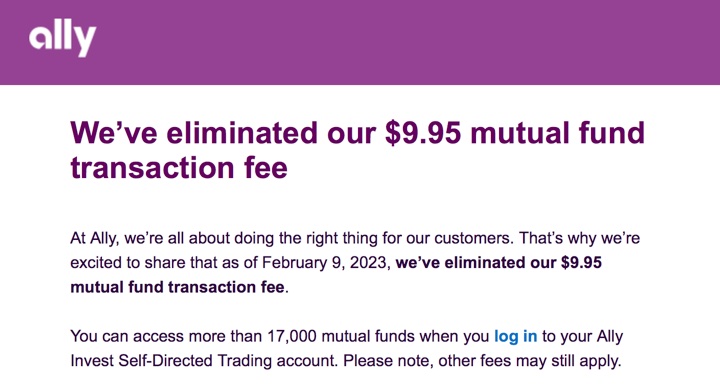

Single-page form for PPP Round 1 loan forgiveness. First of all, if you never took a PPP loan, you can still apply for a first-draw PPP loans under the first-draw eligibility rules. If you already have an outstanding PPP loan, you may have to tried to figure out how to apply for forgiveness through the various Forms 3508, 3508EZ or 3508S. However, if you have a loan under $150,000, there is now a single-page form that requires you to submit to documentation (you must still have it available, of course, and provide it upon request). From the :

The US Small Business Administration (SBA) and Treasury on Tuesday published updated Paycheck Protection Program (PPP) loan forgiveness guidance and forms, including a one-page application for borrowers that received a PPP loan of $150,000 or less.

That form, called the PPP Loan Forgiveness Application Form 3508S, can be used by borrowers that received a PPP loan of $150,000 or less. The form seeks information about the borrower’s loan amount, disbursement date, employee totals, covered period dates, amount of the loan spent on payroll, and the amount of the loan for which forgiveness is being sought. Borrowers are not required to submit any supporting documentation with the application but are mandated to maintain payroll, nonpayroll, and other documents that could be requested during an SBA loan review or audit.

For reference, here is a PDF copy of the (revised 1/19/21). I would still apply through coordination with your PPP lender, which may require a bit more waiting.

PPP Round 2 loan applications now open. Second-draw PPP loans have a different set of eligibility rules. If you are a self-employed worker with no other employees and have higher than a $100,000 net income (2019 IRS Form 1040 Schedule C line 31 or equivalent), then you are completely ineligible for a 2nd draw loan. If you are a self-employed worker and have a least one employee, then the next general hurdle is that you must show a 25% drop in income when comparing the same quarter in 2019 and 2020:

Applicant must demonstrate that gross receipts in any calendar quarter of 2020 were at least 25 percent lower than the same quarter of 2019. Alternatively, Applicants may compare annual gross receipts in 2020 with annual gross receipts in 2019 if they were in business in 2019.

Here are the .

Still looking for a PPP lender? I would start with your existing small business banking relationships, but here is the . Here is , which includes fintechs.

Looking for a self-employed or small business payroll provider? I want to mention here, as I use them for payroll and saw them create many tools this year to help their users satisfy the PPP documentation requirements and help them take advantage of this relief.

If you sign up for a Gusto payroll account by 1/31, you can get a (my referral link). If you are a single-person company, they have a basic tier that costs only $25 per month, which is much less than the major payroll providers. (You can also split up your direct deposit however you like, handy for various banking promotions.)

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2004-2021 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.

Related Posts